SCI CGI — Certification in General Insurance

Certification in general insurance — BCP, PGI, COMGI.

SCI CGI — Performance Analytics

Pass Rate (First Attempt)

98.8%

Based on self-reported first-attempt results from 11,000+ premium users

Score Distribution

Typical Study Progress

Average score improvement over 6 weeks

Topic Coverage Strength

4,009+

Total Questions

98.8%

Self-Reported Pass Rate

30–40 hrs

Avg. Study Time

March 2026

Last Updated

Full SCI CGI Dashboard

4,009+ questions · 10 topics

Final Mock Exam

Full simulation · Timed

AI Tutor

30 questions/day — Popular & Best Value

MathSprint™

Financial math drills

FSRS™ Spaced Repetition

AI-optimized review

Key Study Notes

Condensed summaries

Learn More About Our Offer

Exam Syllabus Topics

Premium syllabus coverage for SCI CGI

General Insurance Fundamentals

Principles and Concepts of Insurance

Personal Lines Insurance Products

Commercial Lines Insurance Products

Insurance Regulatory Framework

Underwriting Practices

Claims Management and Settlement

Insurance Distribution Channels

Risk Management

Professional Ethics and Compliance

Choose the study window that fits your timeline

Choose the plan that fits your timeline and start studying today.

SCI CGI — Certification in General Insurance

Last Updated: March 2026

4,009+ Premium Practice Questions

30 days access with practice questions, flashcards, mindmaps, video courses, and pass guarantee.

90 days access with practice questions, flashcards, mindmaps, video courses, and pass guarantee.

180 days access with practice questions, flashcards, mindmaps, video courses, and pass guarantee.

One-time payment, no recurring fees

One Year Until You Pass Guarantee

Price Will Be Increased Periodically Without Prior Notice

Begin Your Success in Career

Ace the exam in 30 days or less

Our study materials include thousands of exam-style questions, detailed explanations, and key study notes — everything you need to pass on the first try.

Get Instant Access →

Success At Your Fingertip

Study platform used by 16,000+ candidates

Our full-time content team creates original questions aligned to published IBF and SCI syllabus coverage, study-guide updates, and public format specifications.

Get Instant Access →

Monthly Updated

Gain unique advantage over your peers

Our exam team regularly reviews and updates the question bank to keep pace with the latest exam changes and regulatory updates.

Get Instant Access →

Access with Any Device

One click access

Without the need to download any mobile apps, you can add our site as an icon on any mobile device or tablet. Study on the go with just one click and continue learning to achieve success.

Get Instant Access →

Why CMFASExam

Enormous Exam Bank

Large number of questions to help you memorize all possible exam content

Explanation Provided

Get detailed explanation right after each question to deepen your understanding

Support All Devices

Support all tablets and handheld. Study anywhere, anytime on any device

Until You Pass Guarantee

Free extra access if you do not pass—no exam-result proof required

Bonus Tips

Get the bonus article of: 17 Secret Tips To Improve CMFAS Study by 39%

Syllabus & Format Aligned

Original questions follow published syllabus topics and public format specifications

Frequently Updated

Our exam bank is frequently updated by our examination team

Instant Access

No delivery time and fee needed. Access immediately after payment

Quick Reference

Instant explanations after every question

CaseCracker™ Scenarios

Original case-based practice aligned to published syllabus topics and format specifications

Premium Support

Fast help from our exam support team when you need it

FSRS™ Spaced Repetition

Powered by FSRS (Free Spaced Repetition Scheduler) — more accurate than SM-2 used by Anki. Intelligently retests your weak areas

One Year Until You Pass Access Guarantee

If you do not pass, email us within 1 year of purchase and we will add one free access period matching the duration you purchased.

No exam-result screenshot or other proof is required. This is an access-extension guarantee, so you can return to your study plan without paying us again.

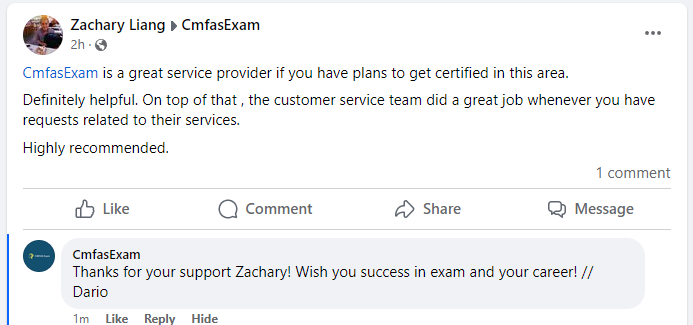

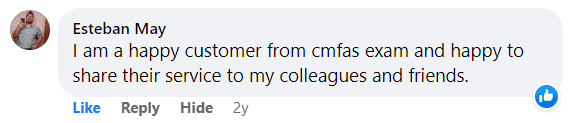

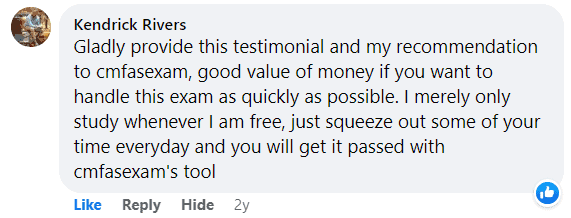

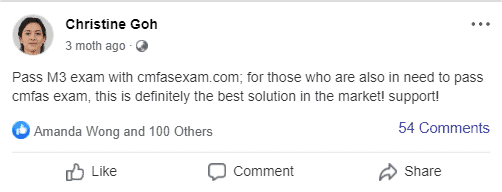

Real Users Feedback

Names are abbreviated for privacy. Some profile images are representative.

Xiang C.

The best part is the detailed explanations. Even when I got questions right, the explanations taught me more.

Mark T.

Quick shoutout to the CMFASExam team — your platform helped me pass 3 modules in 2 months. Incredible value!

Xin S.

Affordable and effective. I compared several options and CMFASExam offered the best value by far.

Jing C.

The guarantee gave me confidence to try it. Turns out I didn't need it — passed easily on my first go!

Haziq M.

Studied for only 10 days using CMFASExam and passed with a good margin. The focused practice really works.

Kumar K.

The best CMFAS preparation tool available. Period. The question bank is extensive and accurately reflects the real exam.

Jia T.

Thank you CMFASExam team! Your service helped me clear the exam that I had been dreading for months.

Faizal W.

My second time using CMFASExam for a different module. Consistently good quality. This is my go-to exam prep now.

Pei O.

My manager was surprised I passed so quickly. The secret? CMFASExam practice questions. Simple but effective.

Gayathri S.

Passed M5 last Friday! The practice questions covered all the key topics. Very grateful for this service.

Si L.

The confidence boost from consistently scoring well in practice exams is invaluable. Walked into my exam feeling ready.

Amanda A.

Great value for money. The question bank is comprehensive and the explanations really help you understand the concepts.

Zhi S.

Just got my results — passed! Can't thank CMFASExam enough. The investment in this platform really paid off.

Faizal H.

Simple, effective, and affordable. Three things that matter most when you're preparing for a professional exam.

Yi A.

Professional service with excellent customer support. Emma was very helpful when I had questions about my subscription.

Shu S.

Passed M9 on my first try! The practice questions were incredibly close to the actual exam. Highly recommend.

Jia T.

Passed on my first attempt with a high score. The practice questions were extremely relevant. Thank you!

Syahirah S.

Passed HI yesterday! CMFASExam was instrumental in my preparation. Highly recommend to everyone.

Jia C.

Very satisfied with the service. The questions are well-written and the platform is easy to use. No complaints at all.

Revathi P.

I've tried other prep services before but CMFASExam is by far the best. The questions are more relevant and up-to-date.

Amirah W.

Five stars from me. Straightforward, effective, and reasonably priced. What more could you ask for?

Mei N.

Clear, concise questions with detailed explanations. This is exactly what you need to pass the CMFAS exams.

Nurul S.

The question bank is regularly updated which gives me confidence that the content stays current with the syllabus.

John W.

This saved me from having to retake the exam. The questions are so well-aligned with the actual test content.

Hui A.

Happy customer here! The platform is well-designed and the content is thorough. Will use for my next module too.

Kai L.

The platform makes studying almost enjoyable. The progress tracking keeps you motivated to finish all the questions.

Sangeetha S.

I appreciate the regular updates to the question bank. Shows that the team is actively maintaining the content.

Li C.

Love the mobile-friendly interface. I could practice questions on my commute which saved me so much time.

Jia C.

Used CMFASExam for M9 and passed on first attempt. Now using it again for my next module. Trustworthy service.

Jun L.

Access was immediate after payment. The interface is clean and the questions are well-organized by topic. Very impressed.

Zi C.

Study notes combined with practice questions make this a one-stop solution. No need for any other materials.

Amirah O.

Used the 90-day plan and had more than enough time. The extensive question bank kept me engaged throughout.

Azman M.

Used the 30-day plan and it was more than enough. Studied seriously for 2 weeks and passed on first attempt.

Hannah T.

Very impressed with the depth of the question bank. Covers even the obscure topics that showed up on my exam.

Michael M.

I was nervous about the exam but after practicing with CMFASExam, I felt very confident walking in. Passed easily!

Aminah I.

Passed first time, all thanks to this wonderful platform. The question bank quality is truly unmatched.

Shi N.

My colleague recommended this to me and I'm glad I listened. Passed my exam last week. Will definitely use again.

Revathi R.

The topic breakdown feature is genius. It shows you exactly where you need more practice. Very data-driven approach.

Faizal S.

I was skeptical at first but the results speak for themselves. Passed M6 with a score well above the passing mark.

Wei K.

Service was excellent from start to finish. Easy signup, instant access, great content, and I passed my exam.

Kavitha B.

I've recommended CMFASExam to at least 5 colleagues. All of them passed. That speaks volumes about the quality.

Jun H.

Excellent resource for busy professionals. I only had 2 weeks to prepare and still managed to pass thanks to this platform.

Mark B.

As a working parent, I needed something efficient. CMFASExam let me study during lunch breaks and still pass confidently.

Revathi N.

The explanations for each question are what sets this apart. Not just answers but understanding why. Very useful.

Wen W.

Great experience overall. The customer support team was responsive and the content quality exceeded my expectations.

Jia C.

Finally found a reliable CMFAS prep tool. After trying others, this one actually delivers on its promises.

Jing L.

Passed with flying colors! The topic-by-topic practice really helped me identify my weak areas and focus my study time.

Amanda J.

The explanations after each question are like having a tutor. Really helps solidify the concepts in your mind.

Danial H.

Just passed CGI! For anyone on the fence, just go for it. The questions are very similar to the real exam.

Li L.

Incredibly helpful for someone changing careers into financial advisory. The questions helped me learn the material fast.

Jia S.

The mind maps helped me visualize complex topics and the flashcards were perfect for last-minute revision.

Michael W.

The variety of question formats really helps. Not just rote memorization but actual understanding of the concepts.

Robert J.

The study dashboard makes it easy to track progress across topics. Very well thought out user experience.

Emily B.

Quick and effective preparation. I spent about 3 weeks practicing and passed comfortably. No need for expensive courses.

Yu C.

As an expat new to Singapore's financial regulations, this platform was essential for my exam preparation.

Syafiq I.

Excellent preparation tool. The questions are challenging enough to prepare you well without being overwhelming.

John B.

My firm reimburses exam prep costs and this was the most cost-effective option. Great ROI on the investment.

Han S.

I was really stressed about the exam but after two weeks of practice on this platform, I passed with confidence.

Matthew W.

The mock exam timer added just the right amount of pressure to simulate the real exam conditions. Very helpful.

Kavitha S.

The mock exams are very realistic. I scored consistently above 80% in practice and passed the real exam with a comfortable margin.

What our users are saying on social media

But Wait… There Is More

After enabling any module, you will also get 6 bonuses For Free

Free Bonus #1 — 101 Resume Writing Tips

After you pass, land the job you deserve. This professional guide gives you a competitive edge in your job applications.

Free Bonus #2 — Video Study Notes

Two sets of audio/video study notes (close to 2 hours each) plus visual mind maps that simplify complex concepts at a glance.

Free Bonus #3 — Beat Information Overload

Master your focus in a data-driven world. Learn strategies to conquer multitasking pitfalls and maximize memory retention.

Free Bonus #4 — Built-in Pomodoro Study Timer

Study using a scientifically proven approach with our built-in Pomodoro timer. Monitor your progress every 25 minutes. Save up to 67% of your study time.

Free Bonus #5 — Interactive Study Mind Map

Stop drowning in manuals; start mapping your success. Our interactive mind map lets you explore exam topics visually — click any topic to reveal sub-topics, key concepts, and connections. Identify knowledge gaps at a glance.

Free Bonus #6 — Study Flashcards

Boost your memory retention with active recall. Flip through 600+ question-and-answer flashcards, navigate with arrow keys or swipe, and master every concept before exam day.

“Can't I Just Study on My Own?”

Of course you can. Any exam can be prepared for independently. But you'll spend weeks extracting key concepts from dense manuals, guessing which topics are actually tested, and hoping you covered enough.

Or you can let our full-time exam team do that heavy work for you — so you can focus on practice, pass on your first attempt, and spend your evenings with friends and family instead of buried in textbooks.

William R. Bennett

CEO — CMFASExam

Our dedicated full-time exam research team

See How Easy It Is — Checkout & Study Dashboard Preview

Watch a quick walkthrough of the checkout process and get a sneak peek at your study dashboard.

Sneak Peek: Your Study Dashboard

Track every question, monitor your accuracy, and watch your mastery grow — powered by our FSRS™ algorithm.

Frequently Asked Questions

Still have questions? Email us at [email protected].

Which CMFAS module do I need to take?

It depends on your profession and licensing requirements. We have a comprehensive guide: visit our "Everything You Need To Know About CMFAS Exam" resource page for a detailed table issued by MAS.

What is the "Until You Pass" guarantee?

If you do not pass, email us within 1 year of purchase and we will add one free access period matching the duration you purchased. No exam-result screenshot or other proof is required.

How does CMFASExam help me pass?

Our full-time content team develops original study materials and question banks from published IBF and SCI syllabus topics, study-guide updates, and public format specifications. We review those sources frequently and update our materials when the published requirements change.

Is the content worth the price?

Absolutely. A failed attempt means paying another exam fee, spending more weeks studying, and potentially delaying licensing or income. Our 98.8% first-attempt pass rate is based on self-reported results from 11,000+ premium users, and every plan includes our Until You Pass access-extension guarantee.

How do I access the content after payment?

Instantly. Once payment is complete, your account is granted full access immediately. Simply log in and start studying.

Will I get the exact same questions as the real exam?

No. To respect IBF and SCI copyrights, we do not copy, reproduce, or reconstruct live exam questions. Our original practice questions are aligned to published syllabus coverage and public format specifications, including Roman numeral I–IV combination questions and standard A–D multiple-choice questions where applicable.

Do all questions come with explanations?

Yes. Every single practice question includes a detailed explanation so you understand the underlying rationale immediately after answering.

Is the content in hard copy or digital?

All materials are digital (online access only). This ensures you always have the latest updated version with no delivery delays. If you prefer offline study, you can print content directly from your browser.

How long should I study to pass?

Study time varies, but generally completing over 70% of our question bank will dramatically increase your pass rate. Many candidates study during commutes and breaks.

Is this a one-off payment or a subscription?

All our plans are strictly one-off payments — there are no recurring fees, no auto-renewals, and no subscriptions. You pay once and enjoy full access for the duration of your chosen plan (30, 90, or 180 days).

Will I receive an invoice for my purchase?

Yes. After payment, an official PDF invoice is automatically generated and available from your Stripe receipt email. You can use this invoice to claim reimbursement from your employer, company, or for tax purposes.

Is my payment information secure?

100% secure. We use Stripe for all transactions. No personal information such as name, credit card number, or address is stored by us.

Are there bulk purchase discounts?

Yes! Purchase two or more modules together and receive an additional 10% discount.

Can my company buy licenses for our team instead of reimbursing employees individually?

Yes. If HR, L&D, or your training manager wants to purchase access on behalf of a cohort, use our self-serve corporate checkout to choose seats, modules, and term in one company order.

View corporate team plansWhat does Premium Support include?

All paid plans include access to our support team for account, billing, and study-platform guidance. If you need help using the materials or planning your revision, just email us and we will assist you promptly.

What is Quick Reference and how does it save me time?

Quick Reference shows you a detailed explanation immediately after each question. You instantly learn what is correct and why the other options are wrong — no need to scroll through the study manual.

What are CaseCracker™ scenario questions?

CaseCracker™ questions are carefully designed case-scenario exercises that mirror the real CMFAS exam. Each scenario presents a realistic financial situation and tests your ability to apply concepts — exactly the format you will encounter on exam day.

How does Spaced Repetition help me remember more?

Our Spaced Repetition system automatically retests you on concepts you previously answered incorrectly or found challenging. It resurfaces similar questions at strategic intervals, reinforcing your memory without you even realising it.

What is the Exam Readiness Score?

Your Exam Readiness Score is a confidence indicator that tracks your preparation progress across all syllabus topics. It analyses your performance across all practice questions and shows your readiness as a percentage. You only achieve "Ready" status when you have completed all premium practice tests with at least 90% accuracy AND reviewed and corrected every wrong answer. This ensures you are genuinely prepared — not just practised — before sitting the real exam.

Ready to Pass SCI CGI?

Join 16,000+ candidates who have prepared with CMFASExam. Unlock the full 4,009+ question bank.